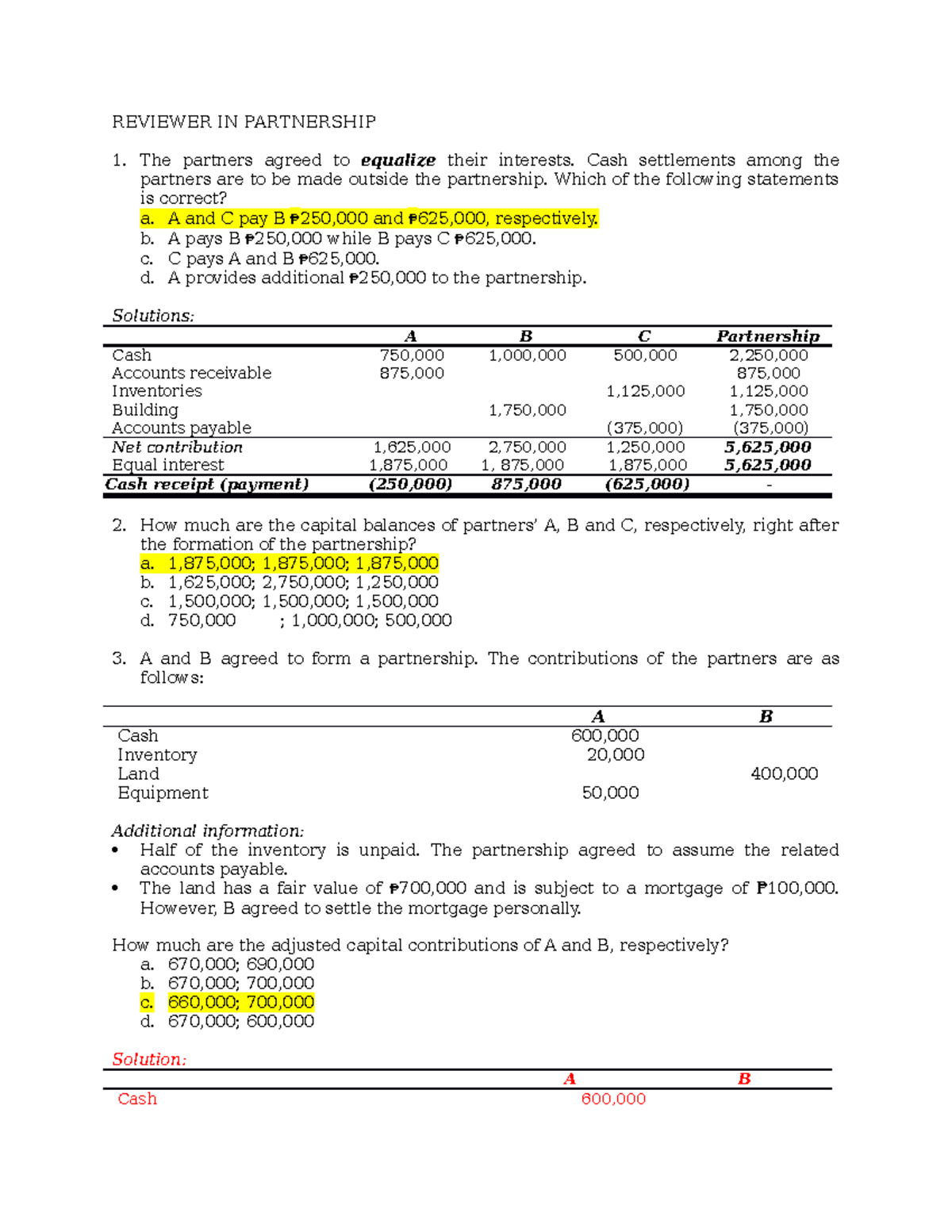

- Have and you may Consult As with any other items within our benefit, likewise have and you will request enjoys a critical impact on costs. If the most people are looking to purchase a house otherwise refinance, rates commonly increase because of the increased consult. If interest levels is actually large and a lot fewer anyone should re-finance or get property, request was lowest while the costs usually slip.

- Interest in Credit Retirement fund and other organization dealers keeps a robust demand for low-exposure borrowing from the bank. Banking companies package private mortages into mortgage-supported securities (MBS) which are ended up selling over to people.

- Federal Treasury Rates Sovereign credit regarding Us bodies is deemed that have zero default exposure, once the Federal Put aside can also be print more cash to blow outstanding expenses. Traders consult a premium more political ties to compensate for home loan pre-money & the risk of standard.

- Inflation & Rising cost of living Requirement Rising prices even offers a big influence on pricing. Since the a savings gets hotter, rising prices will set it. In order to slow rising cost of living, new Federal Put aside will be required to increase rates of interest in order to tigheten borrowing standards. If the a discount are weakening and you may inflation subsides, the fresh Federal Set-aside will then reduce rates. If you are raising or reducing the Federal Fund Rates doesn’t always have a direct impact for the financial pricing, mortgage rates often stick to the government costs over time, and you can usually are some time greater than the speed on ten 12 months treasury cards. While most mortgage loans enjoys a 30-year label, most people often flow otherwise refinance about the 5 to eight ages, this is exactly why the newest finance are indexed contrary to the give towards 10-season treasury notes.

A popular Selection One of Property owners

The brand new 31-seasons FRM is very easily typically the most popular solutions certainly one of each other household consumers and people deciding to re-finance their house money towards the a beneficial lower rates.

If one talks about the market industry general, individuals having fun with fifteen-year FRM so you can refinance helps make the total business structure search good little more even than simply it would instead refis.

Great things about In search of a thirty-seasons Financial

- Repaired Percentage The instant same day payday loans online Alabama original advantageous asset of interested in a 30-year fixed financial is the fact it comes down which have a predetermined fee. Of several consumers before long time have been seduced so you’re able to see a supply which offers a very reduced 1st rate of interest. Immediately following this type of Fingers to switch, of several residents have found themselves in some trouble as they failed to understand exactly how large its commission will be, additionally the the adjusted percentage was unaffordable. Which have a 30-season, you are sure that exactly what your requisite fee could be along side span of the mortgage.

- Generate Collateral An additional benefit out-of finding a thirty-year could it be allows a resident to construct security. Per month, part of the fee happens towards settling the mortgage, which often makes a good homeowner’s home equity. Most other affairs, such as attention just financing, don’t let a citizen to create equity.

- Improved Cash flow An alternative advantage of wanting a thirty-year is the fact it increases your hard earned money disperse. When you are a fifteen-season boasts a lower life expectancy rate of interest, the new monthly obligations shall be notably more than a 30-seasons. By the in search of a 30-year, a borrower will save you numerous buck monthly that may end up being committed to higher producing assets, otherwise spent someplace else.

Can cost you to be aware of

If you’re there are numerous benefits of selecting a 30-12 months, particular loan providers make an effort to lump a lot more costs away from costs into mortgage. Investing closing costs was fundamentally inescapable, as you have to afford bank’s costs & people who show you’ll find «no settlement costs» typically roll this type of will cost you toward financing thru a high desire rate.